Volatility within the crypto world is both the biggest appeal and equally the biggest detractor for its adoption.

Speculative investors are titillated by an asset class that they can invest a small section of their portfolio into a situation where they will conceivably either lose or win in a significant way. A motley crew of believers and opportunists. The obvious problem with this, however, is that this is far closer to gambling than it is to sound investment strategy.

Bitcoin and by extension crypto assets were never designed to be an instrument for speculation and gambling, yet even in a bear market as we are currently in this is what has happened.

One of the primary reasons for this volatility is liquidity or the lack thereof it.

The lack of buy and sell orders causes the market to fluctuate much more rapidly than usual. Without those extra orders, there’s less to absorb market fluctuations.

The less volatile a market, the better a long-term investment it may make, in the sense that it will prove less risky. If a market is more liquid than another, it enables transactions to be completed with greater ease and leads to more honest pricing.

With this in mind, let's look at some of the traditional analysis of liquidity as it relates to price volatility and how we can design architectures to avoid this using the THORChain protocol and incentivizing liquidity.

The five characteristics of liquid markets

In 2002, Tonny Lybek and Abdourahmane Sarr published “Measuring Liquidity in Financial Markets,” an overview of measurements and applications of financial liquidity. They note that there are five distinct factors to consider when it comes to the liquidity of a given asset:

Tightness. This refers to low transaction costs, including (but not limited to) the bid-ask spread.

Immediacy. The speed at which orders are executed and settled.

Depth. The number of limit orders filling out the order book for that asset.

Breadth. A high number of large orders.

Resiliency. A quality of a market in which new orders flow in to correct imbalances and keep the price of an asset closely related to its fundamentals.

Traditional methods of calculating liquidity

Also in “Measuring Liquidity in Financial Markets,” Lybek and Sarr provide an overview of indicators that can be used to illustrate and analyze liquidity developments in financial markets.

Two in particular are worth noting here:

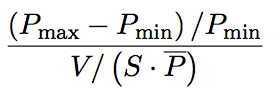

1. The Hui-Heubel Liquidity Ratio. Introduced by Baldwin Hui and Barbara Heubel in 1984, this is a way of calculating the breadth of the market for an asset: the asset’s liquidity increases as breadth increases. This ratio is defined as follows:

In this equation, P Max is the highest daily price over the last five days, P Min is the lowest daily price over the last 5 days, V is the total dollar volume traded in the last 5 days, S is the total number of shares outstanding (i.e. the number of shares held by all shareholders), and P Bar is the average closing price over the last 5 days. As the Hui-Heubel Liquidity Ratio decreases, the breadth of the market — and, with it, liquidity — increases.

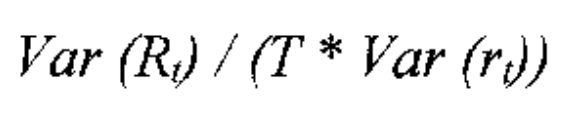

2. The Market Efficiency Coefficient. Proposed by Joel Hasbrouck and Robert A. Schwartz in 1988, this coefficient is meant to describe the difference between long-term and short-term fluctuations in an asset’s price. In this way, it can give us a sense of the resiliency of the asset. It is defined as follows:

In this equation, Var (Rt) is the variance of the asset’s returns over a relatively long-term period, Var (rt) is the variance of the asset’s returns over a relatively short-term period, and T is the number of short-term periods contained in one of the long-term periods. A more resilient — and therefore more liquid — asset will have a market efficiency close to 1.

What is the relevance of this to crypto?

Some of this might seem unnecessarily complex and unrelated to decentralized liquidity network, but it stands to reason that traditional markets have placed this much emphasis on the study of liquidity because of the correlating relation it has to economic stability.

Crypto can never hope to be used transactionally, with any certainty, unless it can reach a price equilibrium.

People often say that BTC is not a currency, but a store of value (SoV), a digital gold. However, this is just an excuse for price instability. Gold does not see price ramps like this, in either direction, which is why it is such a safe investment.

Crypto is obviously not as defensible as gold currently, but at the very least we understand the market forces that we need to incentivize in order to create a more stable trading environment.

Unfortunately, these segmented pools of liquidity which are held in centralized exchanges is not only dangerous (single point of failure/honeypots of assets) but counter-productive to creating a liquid marketplace.

Solving Liquidity

Decentralized exchanges are notorious for having low or zero liquidity to the point where they can be unusable for low liquid pairs.

This can also be the case for low-tier centralized exchanges.

Bancor introduced the concept of continuous liquidity by using smart tokens and connectors built on smart contracts deployed on Ethereum. Tokens and Ether are held in smart contracts in such a way that they become bonded and are priced according to the ratio at which they are held.

As a result, liquidity is “always available” for these tokens. THORChain integrates an on-chain liquidity strategy; termed Continuous Liquidity Pools.

Incentivised On-chain Liquidity

Creating the incentives for on-chain liquidity is a cornerstone feature of THORChain.

Instead of digital assets being held in accounts that don’t contribute to market liquidity, THORChain encourages users to stake their assets in on-chain continuous liquidity pools that add to market liquidity and earn their holders a return.

Continuous Liquidity Pools

Continuous liquidity pools (CLPs) work by bonding two assets to each other in a pool in terms of their value.

Each time an asset is placed in the pool, the opposite asset is emitted in a ratio that matches the corresponding change in value.

As such, trading across a pool creates a price slip which serves as the basis for arbitrage, staking incentivization and price predictability in the pool.

The price slip is mathematically defined, and works to ensure four aspects:

Value always matches across the pool, no matter how large or small an asset pool is.

The trade price is mathematically defined and predictable ahead of time.

Those staking the underlying liquidity always earn a return on a trade.

Those arbitraging across the pool earn a return on a trade.

Architecture towards liquidity

All network architecture of THORChain has been designed to address available liquidity through staking and incentivization. This has been done because we are consciously aware that global currencies cannot function without global pools of liquidity.

Currently, we have fragmented smaller pools of liquidity all over the world — our aim is to connect these pools of liquidity to create a connected stream of available market depth.

Only when this problem is solved, can we hope for any sort of price equilibrium and wider adoption for crypto to be used transactionally.

Stay in Touch

To keep up to date with the Token Generation Event and Airdrop, please monitor community channels, particularly Telegram and Twitter.

- Github: https://github.com/thorchain

- Medium: https://medium.com/thorchain

- Twitter: https://twitter.com/thorchain_org

- Reddit: https://reddit.com/r/thorchain

- Telegram Community: https://t.me/thorchain_org

- Telegram Announcements: https://t.me/thorchain

Related articles

![A technical deep dive into the May 2026 THORChain exploit, explaining how the vulnerability was executed and how it was mitigated.]()

Aug. 6, 2026

THORChain Exploit Report #3

- Report

![Rujira banner announcing 18 new trading pairs on RUJI Trade with abstract purple liquidity routes.]()

Aug. 5, 2026

18 New Trading Pairs Are Now Live on RUJI Trade

- App-Layer

![Ecosystem Update Podcast with Depouch]()

Aug. 1, 2026

Inside depouch: Direct THORChain Swaps Built for Simplicity

- Podcast

![Rujira banner announcing multi-collateral borrowing in RUJI Money Market.]()

Jul. 30, 2026

Multi-Collateral Borrowing Is Live on RUJI Money Market

- App-Layer

![Monero Gets a Soft Launch as THORChain's v3.20 Enters Testing and ADR31 Passes]()

Jul. 30, 2026

Monero Gets a Soft Launch as THORChain's v3.20 Enters Testing and ADR31 Passes

- Podcast

![ADR031 - The Path Forward With Rujira]()

Jul. 29, 2026

ADR031 - The Path Forward With Rujira

![Rujira overview showing native-asset trading, automated trading, lending, borrowing, and liquidations built on THORChain.]()

Jul. 28, 2026

THORChain and Rujira: A Shared Foundation for Omnichain DeFi

- App-Layer

![THORChain and Pirate Chain podcast thumbnail featuring anarchy_dot_gov, KentonC137, and Patriotsounds discussing $ARRR listing on THORChain]()

Jul. 25, 2026

Pirate Chain Wants Off Centralized Exchanges: Next Ask Is an $ARRR Pool on THORChain

- Podcast

![THORChain ADR-029 article thumbnail explaining the REVSHARE mechanism, how the protocol pays affiliates from its own swap revenue and what that means for partner onboarding and quote competitiveness.]()

Jul. 24, 2026

ADR-029 Affiliate Revenue Share

- Report

![Rujira graphic introducing RUJI Money Market as a system for lending, borrowing, and bidding on liquidations.]()

Jul. 23, 2026

How RUJI Money Market Connects Lending, Borrowing, and Liquidations

- App-Layer

![THORChain Podcast #219 thumbnail.]()

Jul. 23, 2026

Dynamic Fees Take THORChain From 6% to 33.5% of ShapeShift Volume, With ADR29 Rev-Share Up Next

- Podcast

![THORChain is transparent even with privacy coins thumbnail.]()

Jul. 21, 2026

THORChain Is Transparent Even With Privacy Coins

- Guide

![THORChain x Liquidy Ecosystem Podcast #218 thumbnail.]()

Jul. 18, 2026

Inside Liquidy’s $700K Treasury: Market Making, Governance and Smarter Rujira Swaps

- Podcast

![THORChain Q2 2026 report thumbnail.]()

Jul. 17, 2026

THORChain Quarterly Report - Q2 2026

- Report

![THORChain Community Podcast #217 thumbnail featuring Devel, Boone, Kenton and Patriotsounds discussing base-layer limit orders, Monero's final review stage and post-exploit volume recovery.]()

Jul. 16, 2026

Devel's Limit Orders Could Make THORChain Swaps Up to 4x Cheaper, at No Cost to the Protocol

- Podcast